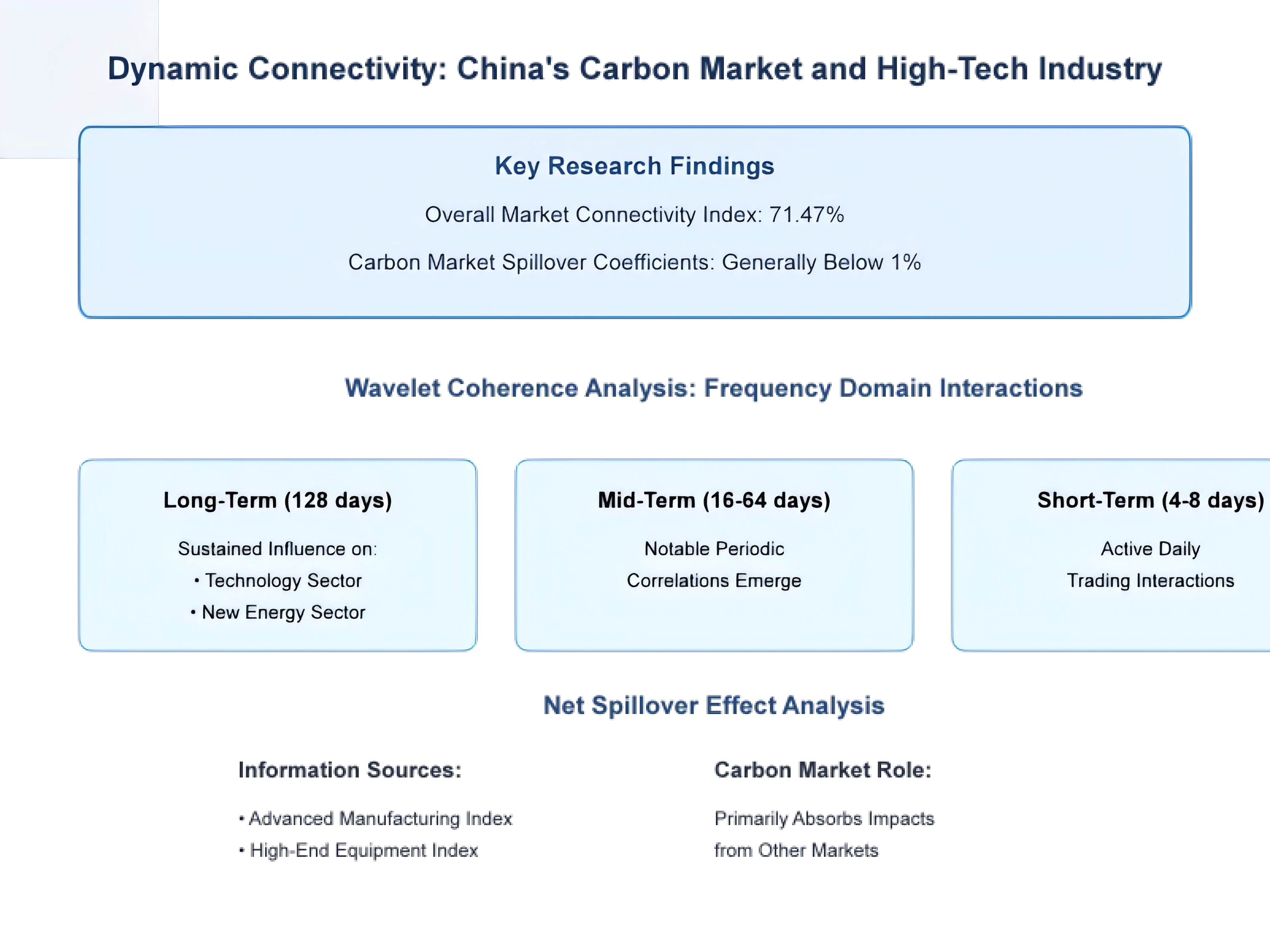

This study utilizes the Time-Varying Parameter Vector Auto-Regression (TVP-VAR) Connectedness model and wavelet coherence analysis to investigate, for the first time, the dynamic connection between China's carbon market and high-tech industry. The results show an overall market Connectedness index of 71.47%, indicating significant information transmission across markets. However, the carbon market exhibits relatively independent characteristics, with spillover coefficients generally below 1%. Dynamic analysis reveals that market Connectedness fluctuates between 60% and 70%, with a narrowing range of fluctuation observed since 2023, suggesting the market's increasing maturity. Wavelet coherence analysis highlights interaction characteristics between the carbon market and various sectors over different time scales: in the long-term frequency domain (128 days), the carbon market exerts sustained influence on sectors such as technology and new energy; in the mid-term frequency domain (16-64 days), notable periodic correlations emerge; and in the short-term high-frequency domain (4-8 days), active daily trading interactions are evident. Net spillover effect analysis demonstrates that the Advanced Manufacturing Index and High-End Equipment Index act as primary sources of information transmission, while the carbon market primarily absorbs impacts from other markets. These findings have significant policy implications for improving carbon market mechanisms, promoting low-carbon industrial transitions, and fostering high-tech industry development. They also provide valuable references for investors in asset allocation and risk management.

{kind=link}