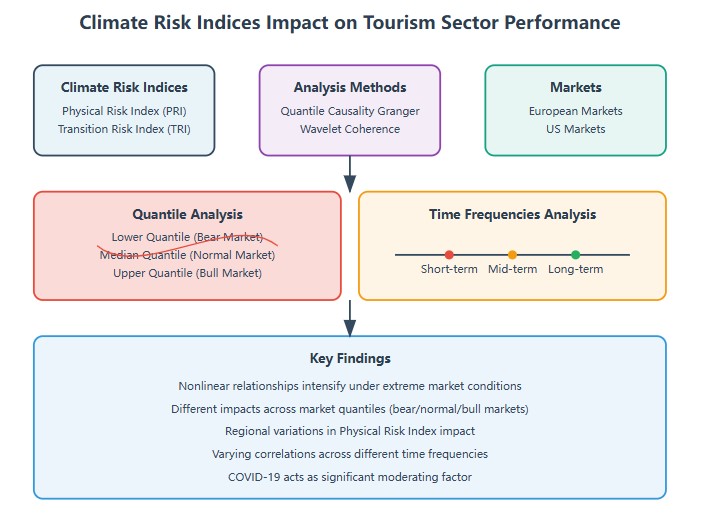

This study investigates the dynamic relationship between climate risk indices and tourism sector performance in European and US stock markets, aiming to understand how climate-related risks affect tourism industry valuations across different quantiles and time frequencies. We apply the Quantile Causality Granger and wavelet coherence methods to examine both linear and nonlinear relationships between the Climate Physical Risk Index (PRI), Transition Risk Index (TRI), and tourism sector stock performance from 2015 to 2022. Our findings reveal a complex nonlinear relationship between climate risk indices and tourism sector performance, which becomes particularly pronounced under extreme market conditions. The analysis demonstrates that PRI impacts exhibit regional variations and temporal dynamics, with significant correlations observed across multiple time scales - from short-term fluctuations to long-term trends. Similarly, TRI shows diverse correlation patterns across different time horizons, with varying degrees of association in short-, mid-, and long-term frequencies. The study also identifies the COVID-19 pandemic as a significant moderating factor in this relationship. Our results provide crucial insights for investment decisions and policy formulation in the tourism industry, highlighting the need for adaptive strategies that account for both immediate and long-term climate-related risks in different regional contexts.

{kind=link}